| LEGAL

DISCLAIMER I am not a Tax Lawyer, Nor do I play Dan Evans on the internet. I am not a Certified Public Accountant, Nor do I play Paul Thomas on the internet. I am not an Enrolled Agent, Nor do I play Richard Macdonald on the internet. DO NOT TAKE MY WORD FOR ANYTHING ON THIS PAGE. Go look it up for yourself. |

2 of 6 Questions, AbridgedI was one of 1,200 people who sent six questions to John Snow, Secretary of Treasury and Mark Everson, Commissioner of the IRS. (Not a typo. ONE THOUSAND & TWO HUNDRED)

Anybody that doesn't know a thing about the 861 EVIDENCE can still understand the simple logic of the first two questions. Either I am to use 26 USC § 861(b) and 26 CFR § 1.861-8 to determine my taxable income, or I am not.

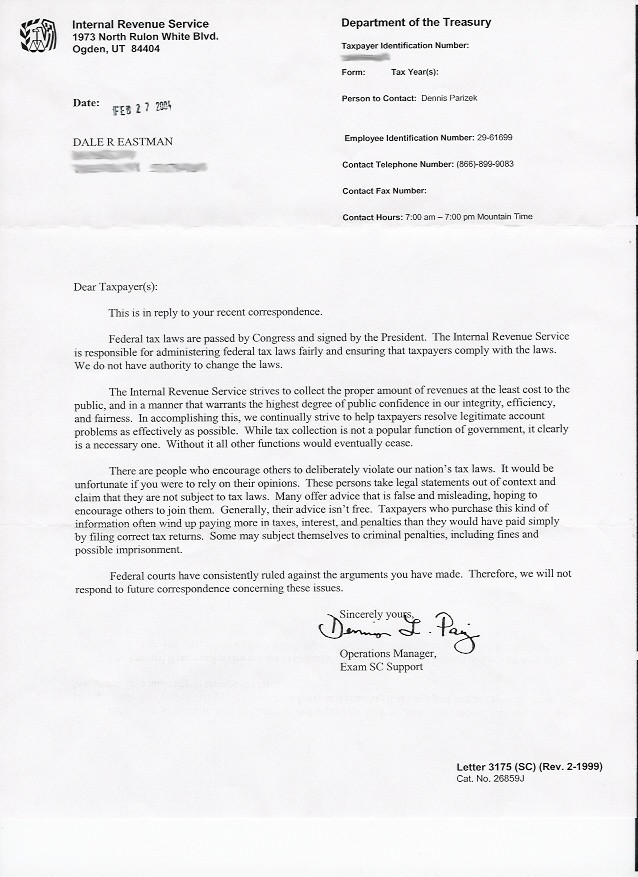

Does the following letter look

like it

was sent by anyone who even read what they were replying to?

|

|

Do you see ANYTHING that even begins to answer yes or no to the first question? Neither do I. With that informative letter in

your mind, check out this exact quote:

Something is incongruous. Something does not fit. Something does not belong in this group.  Which evidence carries more weight?

|